matt_benoit/iStock via Getty Images

Investment Thesis

Chicago Atlantic Real Estate Finance (Nasdaq: NASDAQ:REFI) is a mortgage REIT that lends to state-licensed operators in the cannabis industry. On a valuation basis, REFI is trading at 1.1x P/B and yields 9%, which is not terribly attractive. On a more concerning note, the legal environment provides no margin of safety for cannabis investors, as REFI is not allowed to take title to the underlying real estate while it is being used to conduct cannabis-related activities. Such a statutory prohibition will not allow REFI to realize the full value of the “appraised” value. In addition, if cannabis is eventually legalized, such an event would be detrimental to REFI as larger, more traditional and established players would be able to move into the space.

Background

REFI is a mortgage REIT that completed its IPO in December 2021. It focuses on originating senior (and occasionally mezz) loans to state-licensed operators in the cannabis industry. They are externally managed by Chicago Atlantic REIT Manager and seek to originate loans between $5-200m, generally with 1-5 year terms and amortization when terms exceed 3 years. They typically act as co-lenders in such transactions and intend to hold up to $30m of the aggregate loan amount.

The loans are secured by real estate (when lending to owner-operators) and other collateral (equipment, receivables, licenses, etc.). Some statistics on its current loan portfolio:

-

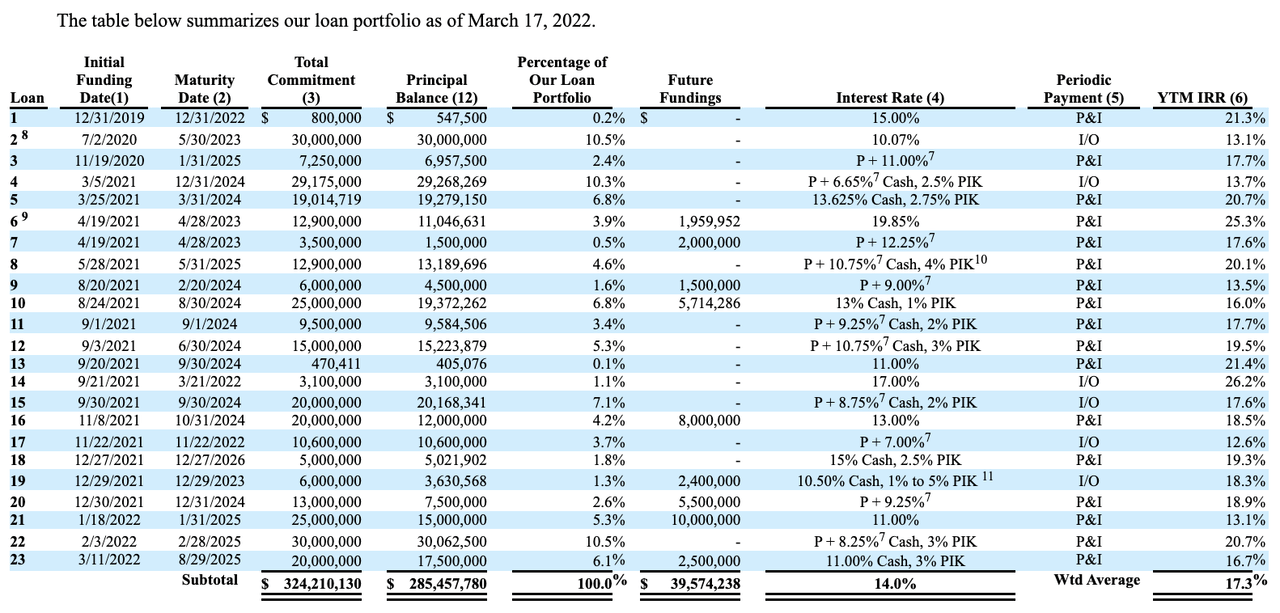

23 loans worth ~$286m, which consists primarily of first mortgages to established multi-state or single-state cannabis operators or property owners

-

Weighted-average yield-to-maturity (YTM) is 17.3%

-

~55.9% consisted of floating rate loans, 44.1% fixed rate loans

-

All loans had prepayment penalties

REFI Current Loan Portfolio (2022 10-K)

The stock is currently trading at $17. With ~17.7m diluted shares outstanding, the market cap/enterprise value (no debt and minimal cash of ~$6m) is ~$300m.

Risks

-

Mortgage REITs: mREITs are in general riskier and prone to volatility; mREITs are also typically leveraged but it doesn’t seem to be the case here

-

Externally Managed: two potential downsides of being externally managed are that (1) less likelihood to achieve economies of scale (management/incentive fees grow just as fast as AUM + required payout of majority of earnings as dividends) and (2) potential conflict with shareholders (e.g. may issue shares below intrinsic value for the sake of growth). There also just isn’t enough historical data to see how REFI’s management will do in the future.

-

Asset Mix/Binary Bet on Cannabis: REFI’s assets are primarily in the cannabis space, which don’t offer much diversification in terms of asset class; in other words, you are taking a binary bet on the success of the cannabis space. Keep in mind cannabis is still a Schedule I controlled substance and is not yet federally legal. All sorts of issues stem from the fact cannabis is still illegal: the difficulty in accessing bankruptcy courts, loans to cannabis businesses may be forfeited to the government, etc.

-

Questionable Collateral: a few key points caught my attention:

-

REFI is not allowed to take title to real estate while it is being used to conduct cannabis-related activities due to statutory prohibitions and exchange listing standards. In the event of a default and if REFI decides to take possession, they must first evict the borrower from the real estate, then engage a third party to remove all cannabis from the property before taking possession.

-

Of course, REFI could pursue other paths in case of default, such as forcing a sale of the property to another cannabis operator, pursuing a judicial foreclosure through a sheriff’s sale (without taking title to the property), or use the property for non-cannabis related operations.

-

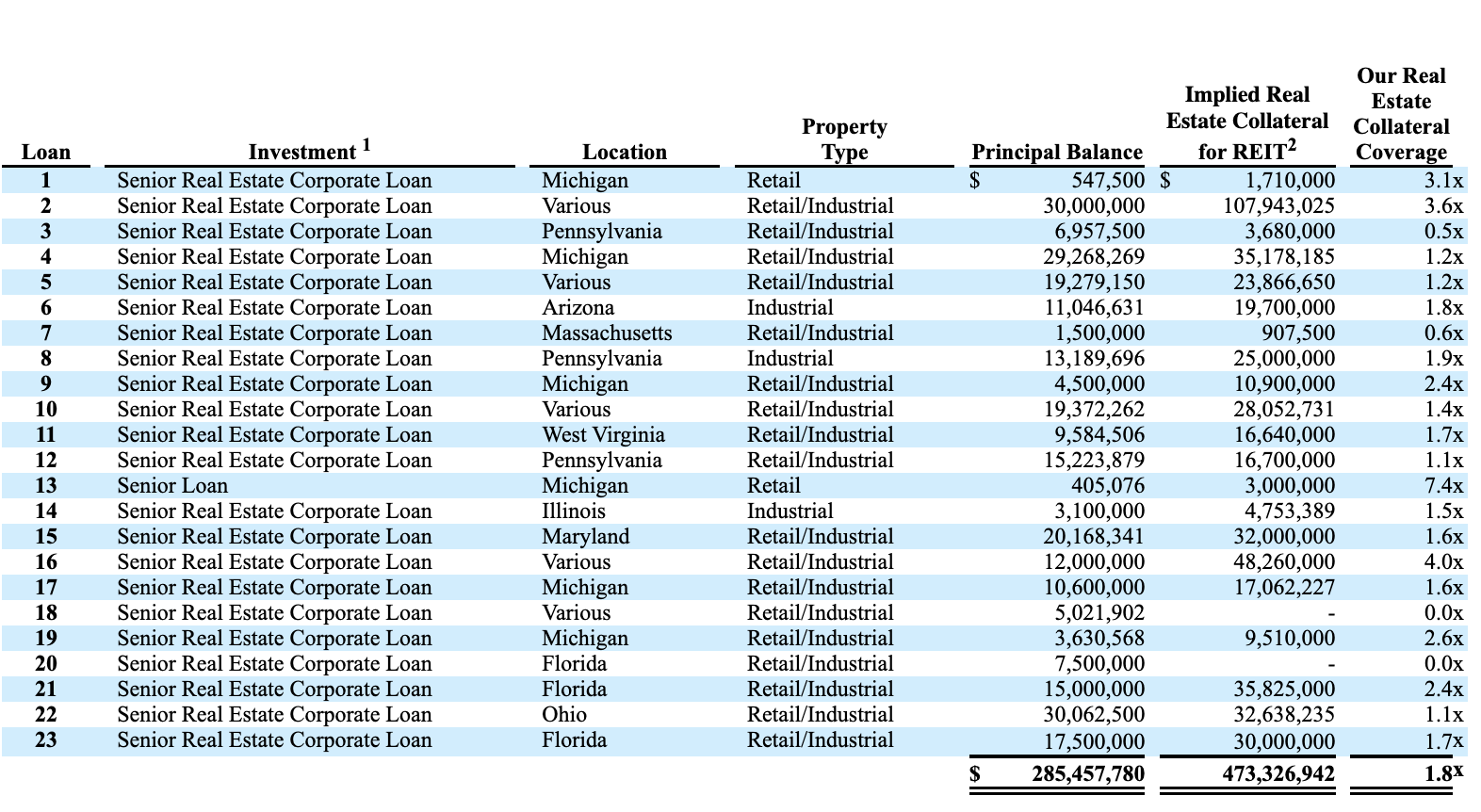

Unfortunately, all the points listed above are value-destructive for the valuation of the underlying real estate. As stated in the 10-K, “Therefore, appraisal-based real estate collateral values shown in the table below may not equal the value of such real estate if it were to be sold to a third party in a foreclosure or similar proceeding.”

- In addition, the appraised values were based on two approaches: income and replacement cost for a similar facility. If you strip out all the cannabis-related “value-add”, then the replacement cost component is rendered meaningless. Which begs the question, “how much is the appraised real estate actually worth?”

-

REFI Real Estate Collateral Coverage (2022 10-K)

-

Rising Interest Rates: we’re currently in a rising rate environment. In such an environment, mREITs earnings generally decline because the cost of money that they borrow to fund their operations increases, which compresses earnings. That is mitigated here since REFI doesn’t seem to have borrowed money. However, the value of the loan will go down if interest rates keep rising.

-

Inflation: in an inflationary environment, you want to be taking on debt (a borrower) and not providing debt (a lender). Why? Because as a borrower, you will be paying back debt with money that is worth less. mREITs are, unfortunately, lenders.

Valuation

Using data from the latest 10-Q:

-

Book Value: $286m in assets, $16.5m in total liabilities → $269.5m in book value (1.1x P/B)

-

Dividend: $0.4/sh for the last quarter → $1.6/sh per year → 9% yield

-

Earnings Per Share (“EPS”): $0.44/sh for the last quarter → $1.76/sh per year (9.65x PE, although not a terribly useful metric since mREIT earnings do fluctuate)

-

Real Estate Collateral Coverage: according to their filings, the loans are secured by real estate value that is worth 1.8x (on average) of the loans; this value is based on their underwriting and is “appraised by a third party at least once a year, or more frequently as needed”. However, I have reservations about the true valuation of the collateral (see my points under Risks- Questionable Collateral). If you decide to impose a 50% haircut (which I normally do in the case of such uncertainty), you get a Real Estate Collateral Coverage of 0.9x.

In short, REFI is trading slightly above book value (1.1x), yields ~9% and its dividend is covered by its earnings. From a valuation perspective, REFI is not terribly attractive; a quick look at BXMT shows that it is trading at 1.1x P/B and yields 8% (roughly the same metrics but with very different risk profiles).

In addition, one key caveat is that the historical performance of a mREIT is an essential component in evaluating them (e.g. trends in P/B, payout ratio, etc.). However, since REFI just completed its IPO less than a year ago, the historical metrics are just not available. Any formulation of value moving forward will be entirely guesswork, which provides zero margin of safety.

Catalysts

-

Insider buying. Two insiders bought in April/May 2022 at $15.50 and $17.95 (~$377k in total). A lot of insiders also participated in a private placement concurrent with the IPO at $16/sh in December 2022 (~$7.5m in total). The shares were subjected to a 180-day lockup that will end on June 5, 2022.

-

Federal Legalization of Cannabis: the legalization of cannabis on a federal level would greatly benefit REFI, but on the flip side, it would also lower the barrier to entry into the cannabis space, paving the way for larger and more established players (which renders REFI’s “edge” moot)

Takeaway

REFI is an interesting company operating in a niche corner of the cannabis industry. In theory, the business makes sense; cannabis operators have limited access to traditional bank and non-bank financing, which allows companies like REFI to make attractive loans to them.

However, on top of being an mREIT operating in a single asset class, its limited historical performance of only 6 months does not allow for the analysis of operating performance. In addition, the inability for REFI to even take possession of cannabis assets as collateral was the “nail in the coffin” moment in my analysis. As a lender, if you are unable to take possession of the underlying collateral, that begs the question- what exactly is backing your loans? The appraised value is partially calculated using a replacement cost of the cannabis facility, which is rendered meaningless if you are forced to strip away everything cannabis-related.

In short, the current legal environment renders no margin of safety for cannabis investors, especially lenders such as REFI. Even if the legal environment changes (e.g. cannabis is legalized), such an action would render REFI’s “edge” useless, as conventional investors/lenders would be free to move rapidly into the space.

From a valuation perspective, 1.1x P/B and a 9% yield isn’t terribly attractive either (on an absolute or relative basis). A quick look at comparable mREITs shows that they are trading similar to REFI but with completely different (and probably more attractive) risk profiles and diversification. In addition, the “appraised” value for the underlying real estate REFI is providing loans for also does not have a margin of safety.

Based on the analysis above, I do not recommend a long position in JJSF (for public short/sell recommendations, like Edwin Dorsey at Bear Cave, I do not hold positions in the stocks I mention and have no intention to initiate a position).